This amazing diagram shows who really runs the Chinese car market (3 photos)

The Chinese car market: major players and structure

The Chinese car market may seem confusing due to the huge number of brands, but detailed infographics help to understand its structure. However, studying this information can raise even more questions.

Who owns who?

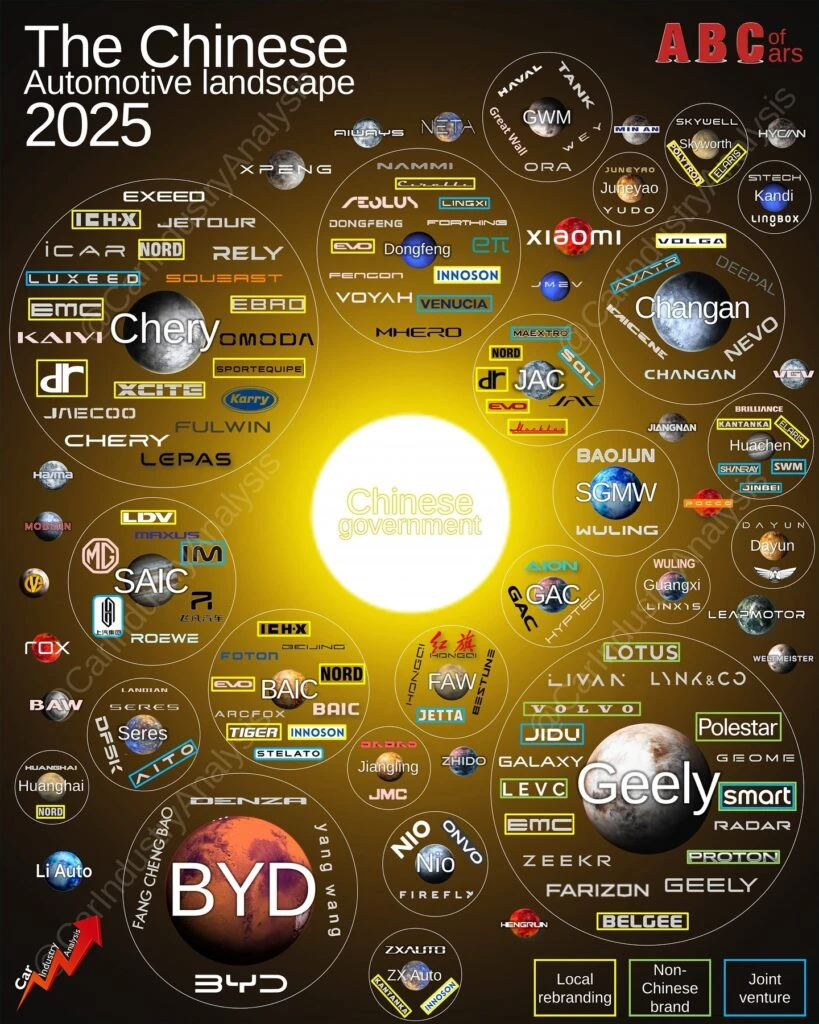

The chart, compiled by analyst Felipe Muñoz, shows all the automakers that are fully or partially owned by Chinese companies. The largest groups by sales in the country are Geely, BYD, Chery and Changan. The latter two stand out in particular because they are state-owned.

Chery Group brands include Fulwin, Omoda, Jetour, Exeed, iCar, Luxeed, Jaecoo, Rely and Chery itself. Changan includes Avatr, Deepal, Nevo, Volga and Kaicheng.

Geely owns or partially controls brands such as Zeekr, Proton, Farizon, LEVC, Galaxy, Volvo, Lotus, Lynk & Co, Polestar, Smart, Geome, Belgee and Radar. BYD’s portfolio is simpler by comparison, comprising its own brand, as well as Denza, YangWang and Fan Cheng Bao.

These four groups account for 56 percent of all car sales in China. They all receive subsidies from the local government, with the companies closest to the “sun” in the diagram having the highest degree of state ownership.

A wider range of manufacturers

In addition to the Big Four, there are other important conglomerates in the market. SAIC owns the MG, LDV, Maxus, IM and Roewe brands; JAC owns Maextro, JAC, Evo and Nord; BAIC includes Arcfox, Foton, Tiger and Stelato; Dongfeng controls MHero, Voyah, Lingxi, Nammi and Venucia.

There are also startups that have so far managed to avoid being taken over by larger groups: Nio, Leapmotor, Xpeng, Aiways, Neta, Xiaomi, Li Auto and Rox. Nio, in particular, has launched the Onvo and Firefly brands.

The Status Brand Pyramid

Muñoz also published a second pyramid chart showing the positions of 109 brands in the market. At the top are ultra-premium brands such as Hongqi, YangWang and Maextro. At the bottom are high-tech contenders such as Xiaomi, Nio and Li Auto.

The premium and semi-premium tiers are filled with brands such as Stelato, Denza, Zeekr and Xpeng, which target status-conscious buyers. The base of the pyramid consists of older, budget brands that are little-known in the West, including Sinogold, Hima, Pocco and others. These brands are in danger of being forgotten as consumers increasingly focus on modern, connected cars.

The Struggle for Survival

It is unlikely that all of these brands will survive in ten years. While the large groups will remain in the market, they may merge or close some of their sub-brands. This trend is already familiar in the West, where brands such as Pontiac, Oldsmobile, NSU, Autobianchi, Sunbeam and hundreds of others have disappeared.

However, it is clear that Chinese automakers are not going to disappear anywhere and will continue to play an important role in the global automotive industry.

The dynamics of the Chinese car market reflect profound structural changes associated with technological development, state support and global expansion. Consolidation and increased competition could lead to the emergence of new global players and the disappearance of less adaptable brands. This process could affect not only the domestic market but also global trends, especially in the electric and innovative vehicle sectors.